[NOTE: Earlier today I testified before the House Budget Committee as part of a hearing on Fulfilling the Mission of Health and Retirement Security. The text of my written testimony appears below. When a link to video becomes available, I’ll put that up, too.]

Mr. Chairman, Mr. Van Hollen, and members of the Committee, thank you for the opportunity to participate in this very important hearing on “Fulfilling the Mission of Health and Retirement Security.”

In the time available, I would like to focus my comments on the health care component of today’s hearing.

Rising Federal Health Entitlement Obligations

A primary objective of the Patient Protection and Affordable Care Act (PPACA) was to increase the health security of the American people. But health security, no matter how well intentioned, will be fleeting if the programs upon which that security depends are unaffordable for taxpayers.

Unfortunately, that is exactly the situation in which we find ourselves today. Federal health entitlement spending has been growing rapidly for many years, and is expected to continue doing so even after enactment of the PPACA. Indeed, it is sometimes said that at some distant point in the future, the long-term rise in federal health care costs will catch up with us. But the truth is that rising federal health entitlement spending has already caught up with us. The budget problems we are experiencing today are directly related to the fact that health costs have risen dramatically over the past four decades. In 1975, the federal government spent 1.3 percent of GDP on Medicare and Medicaid. In 2010, spending on just those two program had risen to 5.5 percent of GDP. That’s more than 400 percent growth.

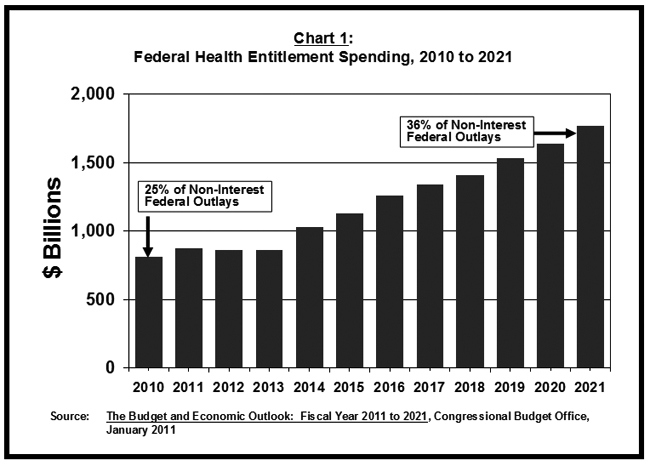

And the Congressional Budget Office’s (CBO) most recent projections show health entitlement spending is poised to rise even more rapidly over the next decade than it has in the past. As shown in Chart 1, CBO expects total health entitlement spending to rise from $810 billion in 2010 to $1,763 billion in 2021. By 2021, health entitlement spending will make up an astonishing 36 percent of all non-interest federal outlays. So more than one in three dollars that the government spends on programs and agency budgets will go to meeting health entitlement obligations.

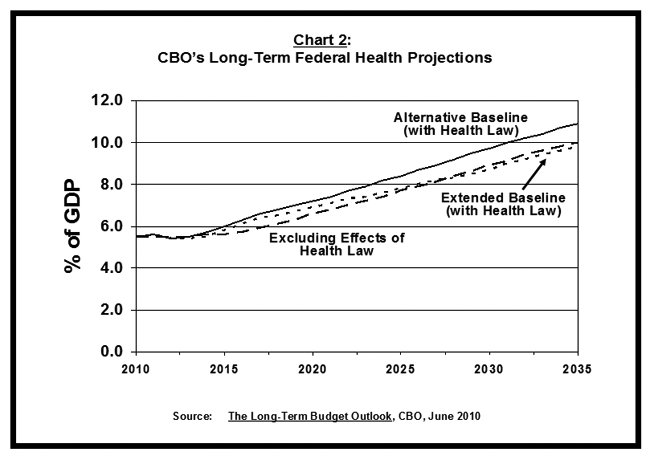

During the debate over the health care law, it was suggested that a goal of reform was to begin to slow the pace of rising federal health entitlement costs. But the PPACA has almost certainly compounded the problem, not solved it. As shown in Chart 2, in a long-term forecast issued last June, CBO estimated what health entitlement spending would be in the coming decades if the health law had not been enacted at all and if it were implemented in full (called the “extended baseline”). With those assumptions, the lines do in fact cross at some point around 2027 or so — meaning the PPACA will have brought health entitlement obligations below the level they otherwise would be. But the “extended baseline” scenario assumes the new law’s deep payment reductions in the Medicare program can be sustained on a permanent basis. As this committee heard at a hearing in January, the chief actuary of the Medicare program believes that to be a very unlikely scenario. Accordingly, CBO has also done a projection of what federal health entitlement obligations will be in future years under the PPACA if the Medicare cuts are moderated even slightly. With that assumption, the PPACA does not reduce federal health entitlement obligations but increases them, by about 1 percent of GDP by 2035.

The Role of Existing Government Policy

Why are health care costs rising so rapidly? The prevailing view has been that the federal government’s health programs experience rapidly rising costs because they are victims of the runaway cost train that is pulling the entire system down the tracks at too fast a rate. According to this way of thinking, the only way to slow the government’s costs is to slow the whole train. That’s the point of view that informed much of the writing of the new health care law.

But this thinking misses a crucial point. Yes, one aspect of cost escalation is an exogenous factor. Rising wealth and medical discovery are fueling the demand for more and better treatments. That should not be resisted in any event. But there is widespread agreement that costs are also high and rising because of waste and inefficiency — and here the problem is not some force outside of government’s control but existing governmental policy.

At present, the vast majority of Americans get their health insurance through one of three sources: Medicare, for the elderly and disabled; Medicaid, for low-income households; and employers for the working-age population and their families. In each of these instances, the federal Treasury is underwriting rapid cost escalation because there is no limit to what Uncle Sam will pay.

In an important 2006 study, Amy Finkelstein, an economics professor at the Massachusetts Institute of Technology, estimated that about half of the real-cost increase in health care spending in the United States from 1950 to 1990 can be attributed to the spread of federally-subsidized and expansive third-party insurance through the government and employers.[1]

Medicare’s important influence on how health care services are delivered is often overlooked or understated. Medicare is the largest purchaser of services in most markets today. Four out of five enrollees are in the traditional program, which is fee-for-service insurance. That means Medicare pays a pre-set rate to any provider for any service rendered on behalf of a program enrollee, with essentially no questions asked. Nearly all Medicare beneficiaries also have supplemental insurance, from their former employers or purchased in the Medigap market. With this additional coverage, they pay no charges at the point of service because the combined insurance pays 100 percent of the cost. This kind of first-dollar coverage provides a powerful incentive for additional use. Whole segments of the U.S. medical industry have been built around the incentives embedded in these arrangements.

Congress and the program’s administrators have, without interruption, tried to hold down Medicare’s costs by paying less for each service provided. Those providing services to Medicare patients have responded by providing more services, and more intensive treatment, over time for the same conditions that patients present to them. In most cases, there is no reason for them not to provide higher-volume care. The patients generally do not pay any more when more services are rendered. And the bill is just passed on to the Medicare program — and federal taxpayers.

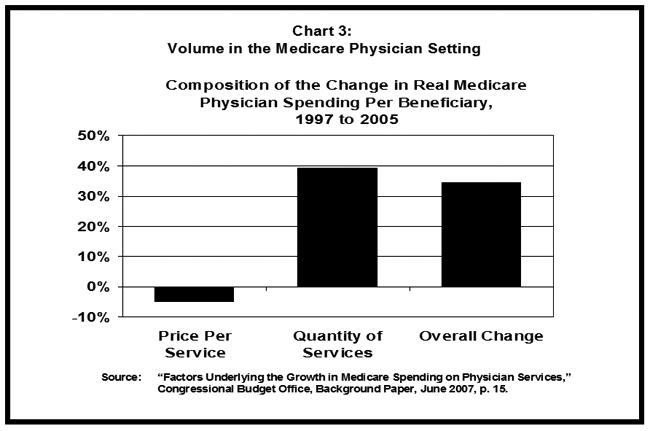

The result of this dynamic is hardly surprising. The volume of services paid for by Medicare has been on a steady and steep upward trajectory for decades. As shown in Chart 3, according to CBO, the real price Medicare paid for physician fees dropped between 1997 and 2005 by nearly 5 percent, but total spending for physician services rose 35 percent because of rising use and more intensive treatment per condition.[2]

Medicaid fuels cost growth because it is financed with a flawed system of federal-state matching payments — with no limit on the amount that can be drawn from the U.S. Treasury each year. For every dollar of Medicaid costs, the federal government pays, on average, 57 percent and the states pick up the rest. In this arrangement, if a governor or state agency wants to cut their state’s Medicaid costs, they have to cut the program by $2.30 to save $1.00 because the other $1.30 belongs to the federal government. Not surprisingly, most state politicians do not find this to be a particularly appealing option. So, instead, they spend most of their energy devising ways to “maximize” how much they get from the federal government for Medicaid services — while looking for creative ways to contribute the required state portion of the funding without really doing so.

The federal tax treatment of employer-sponsored coverage provides a similar incentive for higher costs rather than economizing. Today, employer-paid health insurance premiums do not count as taxable compensation for workers. No matter how expensive the health insurance premium, if the employer is paying, it is tax-free to the worker. Employees thus have a strong incentive to take more and more of their compensation in the form of health coverage instead of cash wages because the health coverage is not taxable. For every dollar spent on health coverage, a worker receives a full dollar of coverage; whereas with every dollar received in other forms of compensation, a portion has to go to the government.

When you put it all together — Medicare’s incentives for rising volume, unlimited federal funding for state-run Medicaid plans, and a tax subsidy for employer plans that grows with the expense of the plan — it is not surprising that health care costs are rising rapidly in the United States. The vast majority of Americans are in insurance arrangements where a large portion of every extra dollar spent on premiums or services is paid for by taxpayers, not them.

The Key Question

So cost escalation is at the center of our fiscal problems, and it is making health care unaffordable for too many people. The key question for health reform is, what can be done about it. Put more precisely, the key question health reformers must answer is this: what process is most likely to succeed in bringing about continual and rapid improvement in the productivity and quality of patient care? Because the only way to slow the pace of rising costs without comprising the quality of American medicine is by making the health sector ever more productive. More health bang for the buck, if you will.

One view holds that the federal government can “engineer” more cost-effective health care delivery. That’s the theory behind the new law’s Accountable Care Organizations, other Medicare pilot projects, the comparative effectiveness research funding, and the new $10 billion Center for Medicare and Medicaid Innovation.

But Medicare’s administrators have been trying for years to change the dynamic in the traditional fee-for-service program and have failed. The problem is that the only way to build a high-quality, low-cost network is to exclude those who are low-value and high-cost. And that’s something Medicare has never been able to do. It’s been much easier, and more tempting, to simply impose across-the-board payment reductions for all providers of services, without picking winners and losers among physicians and hospitals. And so such arbitrary cost-cutting has become the default mechanism for hitting budget targets of various kinds over the years.

And, despite all the talk of “delivery system reform,” that is exactly what was done in the PPACA too. Among other things, Congress enacted a permanent “productivity improvement factor,” which will reduce the inflation increases applied to multiple Medicare payment systems. These reductions will reduce the normal update for the costs of medical practice by about half a percentage point every year in perpetuity for every provider of these services, including hospitals, without regard to how well or badly they treat patients. The compounding effect of such reductions will produce, on paper, enormous savings. But these cuts almost certainly will not be sustained as they will push average Medicare payment rates for services below those of Medicaid by 2019, according to the chief actuary at the Centers for Medicare and Medicaid Services. If that were actually to occur, some 15 percent of Medicare’s hospitals would stop seeing Medicare patients to avoid massive financial losses.[3]

Transforming Health Care Delivery with Cost-Conscious Consumer Choice

There is an alternative to centralized cost-control efforts. It’s a functioning marketplace with cost-conscious consumers.

In 2003, Congress built such a marketplace, for the new prescription-drug benefit in Medicare.

Two features of the program’s design were important to its success. First, there was no incumbent government-run option to distort the marketplace with price controls and cost shifting. All private plans were on a level playing field. They competed with each other based on their ability to get discounts from manufacturers for an array of prescription offerings that are in demand among beneficiaries and their physicians.

Second, the government’s contribution to the cost of drug coverage is fixed and is the same regardless of the specific plan a beneficiary selects. The contribution is calculated based on the enrollment-weighted average of bids by participating plans in a market area. Beneficiaries selecting more expensive plans than the average bid must pay the additional premium out of their own pockets. Those selecting less expensive plans pay a lower premium. With the incentives aligned properly, participating plans know in advance that the only way to win market share is by offering an attractive product at a competitive price because it is the beneficiaries to whom they must ultimately appeal.

This competitive structure, with a defined contribution fixed independently of the plan chosen by the beneficiary, has worked to keep cost growth much below other parts of Medicare and below expectations. At the time of enactment, there were many pronouncements that using competition, private plans, and a defined government contribution would never work because insurers would not participate, beneficiaries would be incapable of making choices, and private insurers would not be able to negotiate deeper discounts than the government could impose by fiat. All of those assumptions were proven wrong. What actually happened is that robust competition took place, scores of insurers entered the program with aggressive cost cutting and low premiums, costs were driven down, and federal spending has come in 40 percent below expectations.

Similar changes — what might be called a defined contribution approach to reform — must be implemented in the non-drug portion of Medicare, as well as in Medicaid (excluding the disabled and elderly) and employer-provided health care.

In Medicare, that would mean using a competitive bidding system – including bids from the traditional fee-for-service (FFS) program — to determine the government’s contribution in a region. Beneficiaries could choose to enroll in any qualified plan, including FFS. In some regions, FFS might be less expensive than the competing private plans. But in some places, it almost certainly would not be, and beneficiary premiums would reflect the cost difference. This kind of reform could be implemented on a prospective basis so that those already on the program or nearly so would remain in the program as currently structured.

In Medicaid, moving toward fixed federal contributions for the acute-care portion of the program would allow for much greater integration between Medicaid and the insurance market available to most workers. Today, when a Medicaid recipient goes back to work, he often loses public insurance but doesn’t get employer coverage. Converting the entitlement into something that can be used in a variety of insurance settings should facilitate portability and more continuous coverage.

For employers, the key is to convert today’s tax preference for employer-paid premiums into a fixed, refundable tax credit that is available to all households (headed by someone under the age of 65), regardless of whether they work or pay taxes. This would provide “universal coverage” of insurance to the entire U.S. population. Any household that didn’t buy coverage would lose the entire value of the credit. The number choosing to do so would likely be very small.

Moving toward a defined-contribution approach to reform would allow for much greater federal budgetary control, which is of course a primary objective and tremendously important for the nation’s economy and long-term prosperity. But this isn’t just a fiscal reform. It’s a crucial step toward better health care too because it would put consumers and patients in the driver’s seat, not the government. With consumer making choices about the kind of coverage they want as well as the type of “delivery system” through which they get care, the health system would orient itself to delivering the kind of care patients want and expect.

Critics argue that this improved fiscal outlook that would flow from moving toward defined contribution health care would come at the expense of the beneficiaries, who would bear the entire risk of costs continuing to rise faster than the government’s newly fixed contribution.

But that would only be the case if building a functioning marketplace had no discernible impact on the productivity of the health sector. It is far more likely that converting millions of passive insurance enrollees into cost conscious consumers will have a transformative effect on health care delivery, and for the better. There would be tremendous competitive pressure on those delivering services to do more with less, and find better ways of giving patients what they truly need. Any health sector player that did not step up and improve its productivity would risk losing substantial market share among seniors, working people, and those on Medicaid. In other areas of our economy that have gone through a consumer revolution, the transformation of the industry has been stunning.

Conclusion

There is obviously much more that needs to be done to ensure a stable and accessible health care system for future generations. Support will need to be limited for those with means so that more can be done for those who need extra help. Special assistance will be necessary to ensure those with pre-existing conditions can secure affordable coverage. And the government will need to do its part, to ensure transparency in prices and quality, and to ensure the rules of the marketplace prevent excessive risk segmentation and inferior care for those with less resources.

But with effective government oversight, cost-conscious consumers have the potential to transform American health care, making it much more productive and of high quality, which is what we desperately need. With such a reform, the system will become more patient-focused, more efficient, and more innovative. The result will be less fiscal stress, a healthier population, and a health care sector that delivers the kind of value the public deserves.